On today’s broadcast, Betterment raises $100 million in fresh capital, Fidelity tests FidelityGo, Schwab pulls the plug on OpenView Integrated Office, and more.

So get ready, FPPad Bits and Bytes begins now!

(Watch FPPad Bits and Bytes on YouTube)

First, a heads up, Steve and I will be on the road later this month covering the massive NAB 2016 event, scouring the exhibit halls for technology you can use to make great videos and podcasts, followed by the 2016 Shareholders Service Group conference in San Diego. Visit fppad.com/subscribe and sign up today so you don’t miss any of our coverage from the events.

Betterment Raises $100 Million from Betterment.com

[Now on to this week’s top story which comes from Betterment, as the automated investment service raised another $100 million dollars in venture capital, bringing the total amount they’ve raised to $205 million. Betterment is pulling away from a crowded field of robo competitors, now servicing over 150,000 customers, managing $3.9 billion in assets, and valued at a reported $700 million.

Betterment says they will use the funding to grow the Betterment for Business 401(k) platform and the Betterment Institutional offering for you, the financial advisor.

But despite all the money raised and what they say about being their customer’s central financial relationship, Betterment’s questionnaire still doesn’t tell customers that they should pay off high interest credit card debt or build up an emergency fund first before investing. Oh, that’s right, customers can find that advice somewhere on the blog.

So I’ll reiterate what I posted on Twitter this week: Betterment, I hope you use the money to make unbiased fiduciary advice accessible & affordable to everyone.

If you want to read more about the latest round of Betterment’s funding, head over to fppad.com/183 for the links to this week’s top stories.] Today marks an important milestone for Betterment and our more than 150,000 customers who have invested over $3.9 billion with us. We’re excited to announce that Betterment has closed a $100 million investment, led by a new partner, Kinnevik.

Fidelity Starts Testing Robo-Adviser Service on Existing Clients from Bloomberg.com

[Next up is news from Fidelity, as the company announced plans to begin testing Fidelity Go, its own automated investing service for retail investors, with roughly 500 customers this week, with an official rollout sometime in the second half of this year.

If you remember back to November of 2015, Fidelity broke off its relationship to promote Betterment Institutional to advisors, and then coincidentally announced the Fidelity Go retail product that competes more or less with Betterment. Fidelity Go will feature investment portfolios managed by Geode Capital Management, all in fees at 39 basis points or lower, automatic rebalancing, but no tax loss harvesting.

With Fidelity Go as a retail offering, you should know that Fidelity told me that a B2B version is under development, and while they couldn’t give me a solid release date, they did say the offering will be customized to your needs as an advisor.

Nevertheless, Fidelity joins Charles Schwab as an institutional custodian with an automated investment solution in the retail space, but at no platform fee in exchange for a little extra cash allocation, Schwab Intelligent Portfolios, in my opinion, is going to be tough to beat.] Fidelity Investments, the second-largest U.S. mutual fund company, will test an automated-investment service starting Wednesday on a small group of existing customers. Fidelity plans to offer the service to the public in the second half of this year.

Schwab Unplugs Its Customized Version of Salesforce from WealthManagement.com

[And speaking of Schwab, this week’s final story is news that Schwab Advisor Services is discontinuing the Schwab OpenView Integrated Office solution effective July 31. Roughly 150 firms are using the solution, so they’re going to have to find some other technology to replace Integrated Office, specifically the custom version of Salesforce that came with it.

The link to the story at fppad.com/183 has the details on options for affected advisors, including using Salesforce with Schwab OpenView Gateway or migrating to a completely new CRM, but here’s the angle I want to focus address.

This is absolutely an example of what can happen when you choose a custodian’s proprietary solution for a part of your technology. How committed is that custodian going to be to offer that technology over the lung run? In this case, Schwab, for whatever reason, is shutting down Integrated Office, leaving 150 advisors with just three months to figure out what to do.

So I don’t blame you one bit for getting a little uneasy when custodians offer proprietary technology solutions to you that they own and control. But with more custodian acquisitions of technology on the horizon, I’m afraid this is a risk you’re going to have to assume more frequently as time moves on.

One more thing: if you want a firm with Salesforce experience in financial services, get your pencils out, because you should consider contacting LiquidHub, Concenter Services, Navatar, Salentica, or AppCrown.] One hundred fifty Charles Schwab advisors must find a new client relationship manager (CRM) by July 31.

Here are stories that didn’t make this week’s broadcast:

Envestnet | Tamarac Rolls Out New Household Structure and Service Team Functionality in Advisor View™ Client Portal from PRNewswire.com

Envestnet | Tamarac has launched four major software updates designed to strengthen RIAs’ online engagement with clients. The roll-out is part of the firm’s March 2016 technology release.

Advyzon Integrates Laser App Software to Enhance Client Advisor Relationship from LaserApp.com

Laser App Software, the premier provider of forms automation and management software for the securities and insurance industries, has announced that Advyzon, an all in one cloud-based platform combining portfolio management, performance reporting, CRM, client portal and planning, integrated with Laser App Software to enhance its client dashboard.

Our team has been hard at work creating the AdvisorQA mobile product experience for Financial Services. It provides a new mobile Content Management and Social Collaboration tool that utilizes the cognitive computing and research capabilities of IBM Watson.

Watch FPPad Bits and Bytes for April 1, 2016

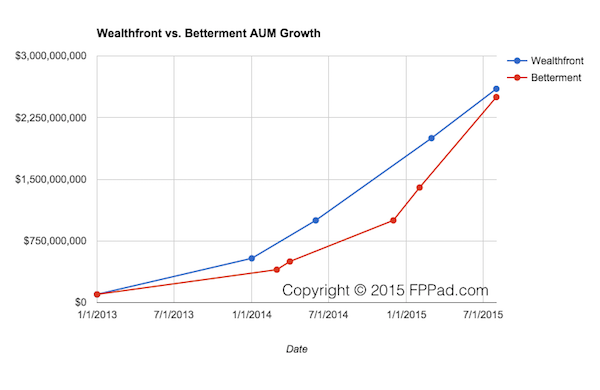

In the race for robo adviser supremacy, neither Wealthfront nor Betterment wants to be runner-up.

In the race for robo adviser supremacy, neither Wealthfront nor Betterment wants to be runner-up.