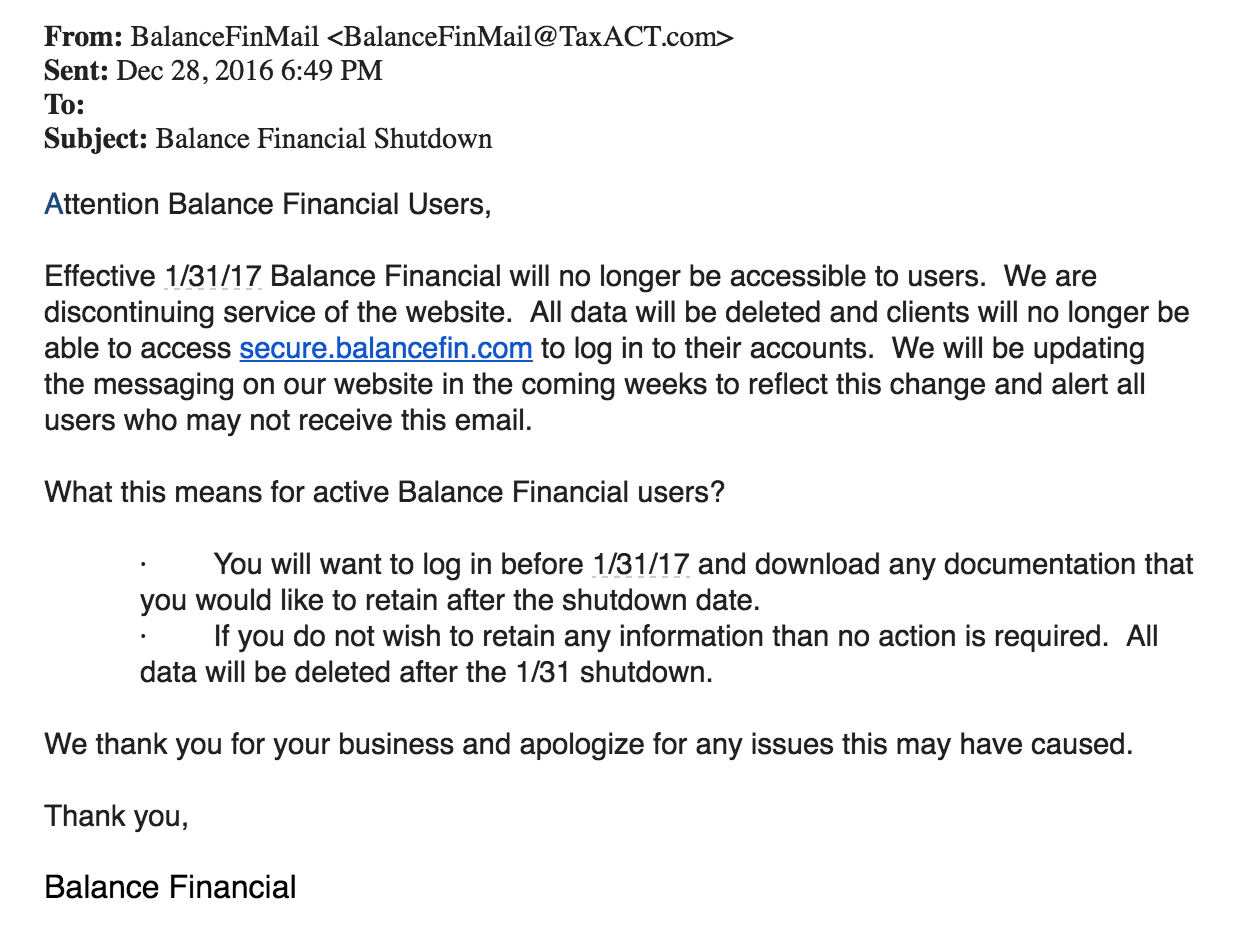

In an email to current users, Balance Financial, a personal financial management app acquired by TaxAct in 2013, announced it will shut down operations on January 31, 2017.

See the email announcement below:

Balance Financial shutdown email announcement sent to users

Balance Financial was an alternative to well-known personal financial management apps, or PFM, such as Mint.com and Personal Capital that performed account aggregation to deliver a consolidated dashboard of a user’s financial accounts.

I listed Balance Financial as a potential alternative for Guide Financial users, but quickly removed it since I had no success in connecting with the company for a statement regarding support for the application in the near future.

Alas, it seems that TaxACT is not interested in supporting Balance Financial beyond January 31, 2017.

I suspect that the number of advisors using the Balance Financial app is very low, likely below a dozen, so few are likely to be affected by the shutdown. What’s less clear is how many retail customers Balance has and what alternatives they find offer similar functionality and pricing to that of Balance.

On today’s broadcast, Schwab announces its Schwab Intelligent Advisory services, Finicity raises $42 million for account aggregation, Envestnet|Tamarac rolls out Yodlee, and more.

Today’s episode is brought to you by eMoney Advisor, featuring a new Client Onboarding process as a part of their leading client experience. Onboarding replaces printed fact-finding documents with an automated, digital workflow, allowing clients to populate their own personal financial information online from anywhere — adding an extra layer of convenience and efficiency to your service.

[Now the big story this week is news from Charles Schwab, as the largest custodian for RIAs announced plans to introduce Schwab Intelligent Advisory™ in the first half of 2017. In the press release, Schwab’s Neesha Hathi said that Schwab Intelligent Advisory is designed for emerging or mass affluent investors who don’t have complex financial situations, features access to CFP® professionals who are available by phone and videoconference, and charges fees of just 28 basis points (disclaimer!) with a maximum of $3,600 a year.

Now this isn’t as much of a technology story as it is a marketing story, because the technology for Schwab Intelligent Advisory portfolio management is that same that powers Schwab Intelligent Portfolios for retail investors and Institutional Intelligent Portfolios™ that you can use in your own RIA if you custody assets with Schwab.

But, how does that make you feel knowing you’re using the same technology that your custodian will use to offer its own human-assisted advisory services to mass affluent clients?

So I was asked if I thought RIAs should be concerned about this announcement, and I said yes, RIAs should absolutely be concerned. Look, when it comes to getting a prospect to buy what you do, most of the time it’s not what you say, it’s what people hear, and I’ve gotta admit, prospects are hearing comprehensive plans by CFP® professionals with 24/7 access, all for 28 basis points (disclaimer!)? Unless your prospects hear something far more different and compelling from you, I just can’t believe they’ll be willing to pay more than three times the price of Schwab Intelligent Advisory for your services.

And I’m not ignoring Vanguard’s Personal Advisor Services, which also employs hundreds of CFP® professionals and charges 30 basis points (thank you!), with more than $40 billion on the platform and growing. A few of you have told me that you’ve lost clients to Vanguard’s service, which is also likely going to happen with Schwab Intelligent Advisory, but the difference with Vanguard is that they’re not also soliciting your custody business while simultaneously soliciting mass affluent clients.

But the executives at Schwab surely know what they’re doing, and I think they know their target RIA client pretty well, which I suspect largely enforces client account minimums of a million dollars or more, so Schwab Intelligent Advisory really isn’t a competitive threat, because it’s not intended for the high-net worth clientele targeted by the largest RIAs that generally choose to custody with Schwab.] Charles Schwab today announced plans to expand its suite of wealth management and advisory services with the launch of Schwab Intelligent Advisory, a hybrid advisory service that combines live credentialed professionals and algorithm driven technology to make financial and investment planning more accessible to consumers.

[Now one of the things not mentioned about Schwab Intelligent Advisory is account aggregation, which is the focus of my next two stories, starting with Finicity, as the company announced it secured $42 million in a new funding round led by Experian.

This is the first time I’ve mentioned Finicity in my broadcast, but I have a popular post on FPPad from March of this year when Intuit announced it was shutting down their Financial Data API and selected Finicity to offer façade APIs to developers who needed to transition off of Intuit’s aggregation.

In the wake of that change, Guide Financial, which was acquired by John Hancock in the summer of 2015, shut down back in October, but other than that I haven’t heard of other significant disruptions among other tech providers.

What remains to be seen is whether or not Finicity makes an attempt to offer aggregation services to advisers, either directly or by partnering with existing technology providers, so if you have some intel you can share with me, I’d appreciate the heads up, otherwise advisers can continue to engage aggregation providers such as Morningstar ByAllAccounts, Aqumulate, eMoney, Quovo Wealth Access, and Envestnet|Yodlee.] Finicity, a leading provider of real-time financial data aggregation and insights, has secured $42 million in new funding. Experian, a global innovator in consumer and business credit reporting, led Finicity’s Series B round, along with a venture debt facility provided by Bridge Bank and participation from existing investors.

[And speaking of Envestnet|Yodlee, my last story highlights the rollout of Envestnet|Yodlee to the Envestnet|Tamarac platform. While at the Schwab IMPACT conference in October, I had a chance to connect with Brandon Rembe to get a quick update on what this new feature means for advisors.

I’ve linked the full interview over here and in the description below, but let me just finish by saying that technology like account aggregation is still a bit of a differentiator for you, since it helps you know as much as you can about your client’s total financial picture, and not just what clients have at one custodian, such as, ohhh, Charles Schwab, which is a complete coincidence.] Envestnet | Tamarac now enables advisors to add assets and liabilities to households in Advisor View™, helping them expand their focus and deliver more holistic advice to clients.

A few parting words:

Before I sign off, you need to know that I have some big plans in the works for FPPad content in 2017. I’m not going to go into the details right now, but what you will notice is that this broadcast, the almost-weekly videos, will be taking a bit of a hiatus for a few months.

But don’t worry, I’ll still be providing my independent insight on financial technology that thousands of you count on as you navigate what I feel is an exciting, unprecedented opportunity in the business of financial advice.

Scottrade® Advisor Services now has agreements with two leading industry solutions providers to help RIAs run their day-to-day routines. Scottrade signed agreements with Morningstar, Inc. and Orion Advisor Services, LLC to offer their services at a discount.

Yahoo, already reeling from its September disclosure that 500 million user accounts had been hacked in 2014, disclosed Wednesday that a different attack in 2013 compromised more than 1 billion accounts.

We recently announced an update to Evernote’s privacy policy that we communicated poorly, and it resulted in some understandable confusion. We’ve heard your concerns, and we apologize for any angst we may have caused.

Advisors have been asking for better ways to visualize portfolio allocations, and we’re excited to announce today that we’re rolling out Asset Class coverage for all portfolios in Riskalyze!

Personal Capital, the leading digital and professional advisor based wealth management firm, today announced that IGM Financial Inc. has completed the firm’s Series E round. Additionally, Silicon Valley Bank has extended $25 million in credit to the firm.

Guide Financial, the financial planning startup acquired by John Hancock in June 2015, told its users via email this week that the company plans to discontinue operations on October 11.

Intuit Aggregation Wake

Guide Financial is the first financial adviser technology provider that I know of that has decided to close its operations in the wake of Intuit’s announcement that it is discontinuing its Financial Data APIs for account aggregation. Those APIs will be maintained only for current production developers until November 15, 2016, Intuit said in an email to developers.

In a phone call with Guide Financial, I learned that the company first attempted to contact as many advisers as possible by phone to communicate the news, and those who were not able to be reached received an email with the details of the shutdown on Thursday.

In the email, the company noted that Intuit had recently announced the discontinuation of the account aggregation services that powered the Guide Financial Service. But in my post from March 2015, How Intuit’s account aggregation shutdown may impact the fintech solutions you use, Intuit told developers that Finicity would be providing façade APIs to facilitate the transition from Intuit to Finicity for aggregation services. Guide Financial did not comment on the option to transition to aggregation provided by Finicity.

No Data Exports

In the weeks prior to the shutdown, Guide Financial users will not have the ability to request an export of their data contained in the system. Generally, data on clients is limited to basic demographic information and is likely to be found in other systems used by advisers, such as CRM and portfolio management software, so an export of that data would not be useful in most circumstances. Guide Financial said that transaction data aggregated from financial institutions will not be made available.

Guide Financial has offered a brief FAQ on its website regarding the transition, and additional questions can be directed to support@guidefinancial.com

Alternatives

For alternatives to Guide Financial, I can think of a few financial planning and financial dashboard solutions that perform account aggregation to update financial plans. The list of the solutions are below:

eMoney Advisor, $1,944 to $3,888/year depending on features, including aggregation and an online client dashboard

Right Capital, under $1,000/year including aggregation

MoneyGuidePro, $1,295/year (I think aggregation is an additional $365/year, but I’m not 100% sure, and clients do not see an online dashboard for their outside accounts)

Note: I originally listed Balance Financial in the list of alternatives above, but I have not been able to connect with them for any updates. Also, their website’s terms and conditions have not been updated for two-and-a-half years (last updated January 28, 2014). Until I connect with someone at Balance, I’ll keep them listed in this note and not as a viable alternative to Guide Financial.

There are other solutions that perform aggregation (ByAllAccounts, Aqumulate, Quovo, Blueleaf, Wealth Access, etc.), but they generally don’t also have financial planning capabilities built directly in to the program.

If you can think of other solutions that should be on this list, contact me (or tweet me @billwinterberg) and I will update this list.

Intuit’s Financial Data API looming shut down will have a ripple effect across popular account aggregation providers

Intuit’s looming Financial Data API shut down will have a ripple effect across popular account aggregation providers

Quick Take:

Intuit is discontinuing its Financial Data APIs widely used for financial institution account aggregation

Account aggregation providers using Intuit feeds (e.g. Blueleaf, Quovo, Wealth Access, Plaid and more) may need to transition to an alternate account aggregation provider

Intuit identified Finicity as a suitable account aggregation provider, but Finicity has issues around its business that raise concern for me

For advisors, your clients will have to reauthorize any accounts aggregated using the Intuit APIs as various companies phase out their use of the Intuit data feed

The API will be maintained only for current production developers until November 15, 2016 to enable time for migration.

In the wake of Intuit’s decision, Guide Financial became the first adviser fintech provider to announce they are shutting down their service later this year. See Guide Financial to shut down operations on October 11.

Intuit identified Finicity as a solution that will provide a “façade” API interface that translates Intuit-structured API calls into Finicity-structured API calls.

Financial Data API Backstory

The Financial Data APIs from Intuit allow developers to link to end-users’ banking accounts from within their application.

In September of 2012, Intuit announced that it was opening up the technology that powered Intuit products like Mint.com, Quicken, and QuickBooks to the developer community via a library of APIs that it called Customer Account Data (CAD).

Customer Account Data, which was rebranded Financial Data APIs, is composed of two separate products: the Transactions API and the Identification API Beta.

The Transactions API offered connections to roughly 20,000 US and Canadian financial institutions, enabling third-party developers to quickly and cost-effectively deploy aggregation functionality to a wide array of financial sources.

The Identification API Beta facilitated customer’s identity and banking account verification using banking credentials. Developers were able to configure ACH connections via the API instead of relying on microdeposits (a series of deposits under $1 that the customer verifies) and a process called “fatfingering.”

FinTech Floodgates

The general availability of the Intuit Financial Data APIs opened the floodgates of all sorts of new B2C fintech startups that featured the aggregation of users’ financial accounts. These startups included popular names such as LearnVest, SaveUp, Hello Digit, BillGuard, and more.

A similar increase has taken place among B2B account aggregation providers, with companies like Blueleaf, Wealth Access, Quovo, Plaid, and Right Capital all appearing with some type of advisor aggregation fintech solution over the last four years.

Prior to the new wave of account aggregation providers, advisor solutions were dominated by four key players:

Yodlee, acquired by Envestnet, completed in November 2015 for $538 million

So now that Intuit is going to shut down access to its APIs, several fintech aggregators should find themselves scrambling for a suitable replacement before November.

Based on my research, many companies I mentioned earlier are going to have to fill the gap left by Intuit’s hole in the marketplace. They include:

Betterment (retail and Institutional, based on their use of both Plaid and Quovo)

Note: Prior to August 30, 2016, I had Right Capital in the list above. After connecting the Right Capital co-founder Shuang Chen, I learned the company had considered Intuit’s API for aggregation at one time, but ultimately decided to engage Yodlee for account aggregation. Therefore, Right Capital will not be affected by the Intuit API shutdown.

In its press release, Intuit identified Finicity as an alternate provider of aggregation services.

We have identified a new aggregation partner, Finicity, for whom this service is a core part of their business. Finicity can offer long-term benefits and service for our aggregation customers. To minimize developers’ engineering work to switch APIs, Finicity will provide a façade API interface that translates Intuit-structured API calls into Finicity-structured API calls.

The “façade API interface” means that developers with existing code that calls on Intuit APIs will not need to change their codebase. Instead, Finicity will publish an API interface that is 100% compatible with existing calls to the legacy Intuit APIs and return data to the developer’s application as if Intuit’s APIs never went away.

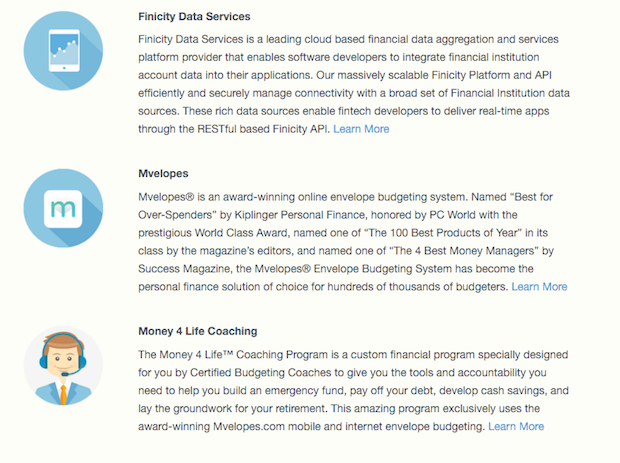

Who is Finicity?

For me, Finicity is a newer name in aggregation that came to my attention last year while monitoring Quora for details on Yodlee despite founding the business in September 2000.

While the Finicity compatibility endorsed by Intuit sounds good for existing developers, there are certainly other issues to consider before building a business on top of Finicity services, and that absolutely should factor into the due diligence process of advisors.

Finicity has a relatively unremarkable profile in CrunchBase, but a few more details about adoption and marketshare come from Finicity co-founder Nicholas Thomas from this Quora question:

2015 has been a good year for Finicity. We’ve signed hundreds of Fintech and Financial Institutions to build their solutions on our API, have quietly launched over a dozen partners, and are launching dozens more in 2016. Our partners tell us that our broad native data source coverage and our fanatical agg support teams are the primary reasons why they love us.

-Nicholas Thomas

So with relatively little marketing (e.g. as I published this, their most recent tweet was on October 27, 2015), Finicity managed to sign up “hundreds” of customers, launched “over a dozen” partners, with more on tap in 2016.

Is account aggregation Finicity’s only play in the industry? No.

To see what other lines of business Finicity offers in addition to their aggregation services, their website lists two other divisions: Mvelopes and Money 4 Life Coaching

Mvelopes from Finicity

Mvelopes is a software application for personal budgeting and has extremely high ratings for its apps in the app stores. Surprisingly high, actually (more on this later).

Mvelopes allows users to create virtual envelopes for different spending categories and allocate money to them accordingly. The idea is that throughout the month, users refer to the amount of money left over in each envelope after paying bills in order to preventing overspending. Transactions are aggregated from connected accounts, and transactions are automatically deducted from applicable virtual envelopes of available cash.

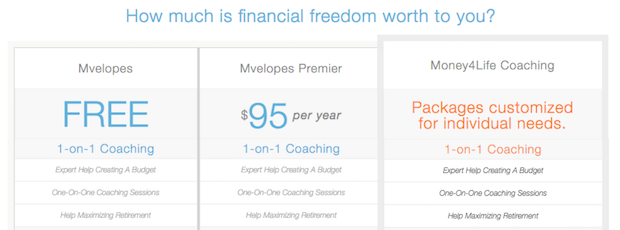

The service is free to use with a limit of four aggregated cash flow and credit accounts (here’s the Finicity aggregation connection). To access unlimited accounts, users subscribe to the Mvelopes Premier plan for $95/year.

Money 4 Life™ Coaching

Where things get more controversial for me is Finicity’s division called Money 4 Life™ Coaching. The Mvelopes pricing page makes the first mention of coaching services and describes how customers can benefit from one-on-one coaching customized for individual needs.

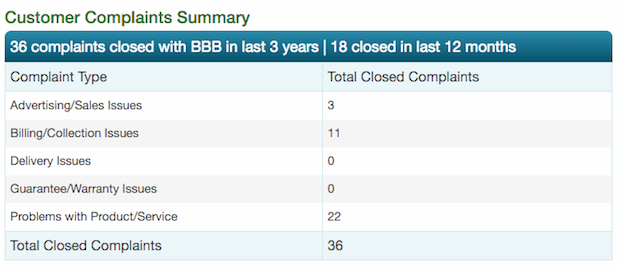

So I looked into this coaching services with a quick Google search and came across quite a few consumer complaints (36 to be exact) about the services on the Better Business Bureau website.

Most of the complaints seem to be centered around the Money4Life coaching including allegations of no contact by coaches for months at a time and allegations of cancellation difficulties.

Most complaints listed on the BBB site appear to reach a satisfactory conclusion once customers initiate the dispute process (which results in an overall BBB rating for Finicity of A+) , but it is surprising that many customers feel that they need to involve BBB in the first place in order to reach a resolution.

Also, the Mvelopes mobile app ratings are overwhelmingly positive, but many of the five-star reviews have no details in the description or come from users with no other app reviews other than Mvelopes. It’s eyebrow raising.

Critical Mvelopes app reviews such as the one below from iTunes are enlightening:

I contacted Finicity for comments and have not yet heard back from the company, so I will update this post accordingly.

What’s Next?

So what’s next? Given Finicity’s connection to awkward customer experiences under the Money4Life coaching program, how likely are the younger aggregation providers to migrate their API calls to the Finicity API? Or will there be a trend to simply abandon the aggregation of financial institutions currently covered by Intuit?

No matter what, as the aggregation vendors make their decisions behind the scenes, advisors’ clients will need to reauthenticate their usernames and passwords once a migration to a new aggregation service is implemented.

For some firms that have a handful of aggregation accounts, this may be a non event, but for larger firms with thousands of aggregated accounts, the issue could take weeks or months to resolve as all clients work through their accounts to reauthenticate their login credentials.

Yodlee, known by financial advisers mainly for its data aggregation services, agreed to be acquired by Envestnet, the wealth management services and technology provider to financial advisers.

Yodlee raised $75 million in an October 2014 IPO after approximately 15 years as a private company, valuing the company around $340 million.

Financial advisers do not directly use Yodlee products or services, but many of the technology services they do use employ Yodlee account aggregation services (see below).

Fiserv’s CashEdge also performs account aggregation and the company sells an advisor-facing aggregation product called AllData Advisor®.

MoneyGuidePro has offered discounted pricing for Yodlee, but now is presented with a conflict given that Yodlee’s new owner also recently acquired Finance Logix, a competing financial planning software solution.

Who Uses Yodlee?

Noteworthy adviser technology vendors who use Yodlee include Blueleaf, CircleBlack, MoneyGuidePro (see MoneyGuidePro to integrate Yodlee for account aggregation), Orion Advisor Services, Wealthminder, Wealth Access, and Wells Fagro.

If you’re Envestnet, or if you use Envestnet products and services in your business, this acquisition is good. Very good. Envestnet now has a very broad portfolio of services that helps financial advisers run efficient businesses.

What services, you ask? They offer CRM, portfolio management and reporting, client portals, business intelligence, and mobile apps from Envestnet|Tamarac, financial planning software from Finance Logix, and now account aggregation from Yodlee.

If you’re a vendor who competes with Envestnet AND offers account aggregation to your financial adviser users, it could be bad. One of your product’s competitive differentiators, account aggregation, just got acquired by a leading vendor of financial technology and portfolio management solutions to advisers. Now what do you do?

And if you’re an adviser who doesn’t use Envestnet, your choices for an independent account aggregation solution are now smaller. Who’s left? Aqumulate, Intuit, Quovo, and Openfinance.

ByAllAccounts is owned by Morningstar (but an important note is that Morningstar doesn’t sell investment products or portfolio services, but rather adviser technology and investment research).

And Intuit is a special case, too, as once again, advisers can’t directly purchase or subscribe to Intuit aggregation. Aggregation from Intuit must be integrated by a third-party technology provider.

Openfinance is one to watch, as I was told recently that First Rate, SunGard’s main performance reporting partner, teamed up with OpenFinance to provide aggregation solutions for First Rate integration partners (e.g. Grendel CRM from Big Brain Works).

Plaid is out there too, but as far as I can tell, their bread-and-butter customers are consumer-oriented financial apps like Acorns and robinhood.

So overall, are the limited choices among aggregation solutions good or bad? I’m not entirely sure.

Some advisers choose not to offer account aggregation at all. Some do. It largely depends on how the business is structured and whether or not account aggregation boosts the overall value proposition of the firm.

A Yodlee Backstory

One of the Achilles’ heel of financial services is the forced fragmentation of where all of us keep our money.

Your monthly income and spending flows through a bank checking account.

Want a savings account that actually has an annual interest rate that isn’t zero? You’ll probably open an online savings account.

Want to invest in low-cost mutual funds? You’ll likely open an account directly with the fund company.

Want to own a few stocks? You’ll need a brokerage account for that.

Want to save for retirement? Your employer requires you to use certain retirement plan providers. Time to open another account.

Want to save for college? Again, your state might have a specific plan sponsor if you want to take advantage of state tax deductions. Boom, another account!

Seriously, why must the industry be so fragmented that consumers have no choice but to open so many discrete accounts across so many financial institutions?!?

So if you’re like most people who live on planet Earth and use money, it’s nearly impossible to see what you have one place AND keep that report up to date as your spending fluctuates and your investments rise and fall.

Enter Yodlee.

Yodlee seized the opportunity among this fragmentation to facilitate all-in-one reporting. As online financial account access became mainstream, Yodlee allows consumers to grant permission to read data from each financial account and aggregate all that disparate data into one dashboard, the Yodlee MoneyCenter. To build a buisness, Yodlee charges third-party companies (e.g. banks, insurance companies, trust companies, broker-dealers, financial apps like Personal Capital and LearnVest) to be on the receiving end of the aggregated data.

Fast forward to today and Yodlee’s market value for its business is in the neighborhood of $660 million.

And now you know the Yodlee backstory (well, as I tell it. There’s a lot more to the story, but this is what matters for you, the financial adviser).

Note: An earlier version of this post suggested that rumors indicated the Fiserv adviser-facing product AllData Advisor® was being phased out. A company spokeswoman for Fiserv wrote, “At this time, Fiserv has no plans to phase out the referenced advisor-facing product.”

Morningstar buys ByAllAccounts for $28 million. What this means for financial advisers and the future of account aggregation.

News hit the wires late yesterday that Morningstar acquired ByAllAccounts for $28 million, subject to working capital adjustments. Read the press release from Morningstar.

“Business As Usual”

In an email to ByAllAccounts subscribers, James Carney, President and CEO of ByAllAccounts wrote, “For now, it’s business as usual. Going forward, we will be evaluating opportunities for closer collaboration with Morningstar in ways that benefit our customers.”

ByAllAccounts has a near monopoly, in my words, in the reconciliation-ready account aggregation marketplace. The company has over 2,100 clients, connections to over 4,300 custodians, and 40 platform and service providers as of the March 2014 acquisition.

ByAllAccounts Alternatives

The other reconciliation-ready provider is Aqumulate, formerly Advisor Exchange, which can be viewed as a value-added reseller (my words again) of the CashEdge aggregation service offered by Fiserv.

See, raw data from Fiserv’s CashEdge isn’t normalized, tech speak for “cleaned up” with usable data that can be imported into portfolio management software like PortfolioCenter from Schwab Performance Technologies®, Black Diamond Performance Reporting from Advent, Orion Advisor Services, and more.

So Aqumulate partners with Fiserv to access their network of over 14,000 financial services companies (more than three times ByAllAccounts’ connections), and then cleans up the raw CashEdge data so it can be easily ingested by advisers’ portfolio management software.

Why Reconciliation-Ready Data?

So ByAllAccounts and Aqumulate are the only two practical solutions for advisers who require reconciliation-ready account data for imports to portfolio management software.

But I see a trend among progressive RIAs who are dropping performance and rate of return calculations for client investment reports, especially among shops who embrace passive strategies of DFA and Vanguard funds.

Why continue to emphasize performance, performance, performance quarter after quarter when it’s a minority piece of the total wealth management framework?

Look at reports from Blueleaf (important distinction: they’re NOT statements) as an example of this trend. And they even use ByAllAccounts for some held away account aggregation!

And then look at the reports offered by the online advice providers with aggregation capabilities: Personal Capital and Learnvest exclusively highlight net worth, cash flow, and asset allocation, all powered by Yodlee aggregation.

But will users find actual statements on total investment portfolio performance?

No.

eMoney operates the same way. Over 90% of its custodial data connections are proprietary, with the remaining connections rounded out by CashEdge and ByAllAccounts, and you won’t find portfolio performance statements anywhere in the program.

Is individual stock and fund performance listed in these programs? In most cases, yes, because those stats come from Xignite and others and are not subject to knowledge of a client’s actual time-weighted rate of return for portfolio performance.

The Household Balance Report Standard

So household balance reporting, and not performance reporting, is gaining momentum, and that segment is being supported by lower-cost providers like Yodlee and Intuit in addition to ByAllAccounts and Aqumulate.

So why should advisers pay thousands to ByAllAccounts when you can get client balance and holding information from Yodlee and Intuit for far less?

Once again, only those who need reconciliation-ready data for performance calculations were cornered into paying a premium to ByAllAccounts or investigating Aqumulate, and I think that population is slowly shrinking.

Did that influence ByAllAccounts’ decision to seek a buyer at the potential top?

Bob Curtis, President and CEO of MoneyGuidePro (right) forecasting the future of financial planning with Harold Evensky (left)

Popular MoneyGuidePro financial planning software to aggregate held away accounts through a new Yodlee integration

Ask most technology consultants and financial advisers about their account aggregation options, and you’ll likely hear just a few common names.

ByAllAccounts, Fiserv’s CashEdge, and perhaps Intuit.

But Yodlee?

That solution almost never gets mentioned.

Until now.

MoneyGuidePro Integrates Yodlee

In a packed general session at the 2014 Technology Tools for Today (T3) conference, Bob Curtis, President and CEO of MoneyGuidePro announced that the popular financial planning software program will soon integrate account aggregation functionality using services from Yodlee.

One of the reasons I believe Yodlee hasn’t gained traction among financial services technology solutions is price. Yodlee is a rather expensive solution relative to its counterparts in the marketplace.

But MoneyGuidePro is breaking down the potential barrier of cost with very aggressive pricing.

Yodlee For $1 a Day

In his general session, Curtis announced that MoneyGuidePro will offer the Yodlee integration at an introductory cost of $365 annually. That’s right, just $1 per day.

And as to when the Yodlee integration will be available, Curtis told advisers that the account aggregation functionality is anticipated to be rolled out in Q2 of 2014.

For more information on the Yodlee integration with MoneyGuidePro, read the full press release at BusinessWire.